Overview

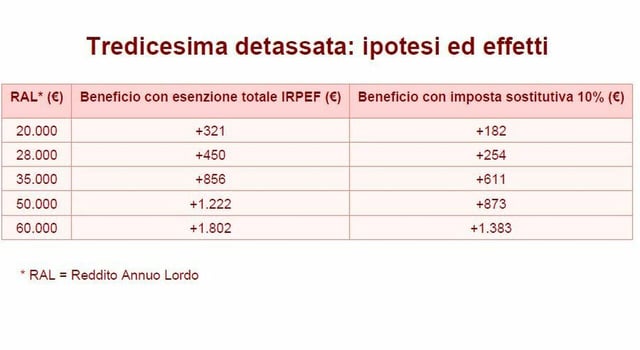

- Two approaches are being discussed inside the governing majority: a full IRPEF exemption on the tredicesima or a 10% substitute tax.

- A complete exemption would require several billion euros in budget cover, whereas a 10% rate is presented as a more sustainable compromise.

- Currently the 13th-month payment is taxed under ordinary IRPEF without employee deductions and also incurs roughly 9.19% in social contributions.

- Illustrative calculations show a worker earning €30,000 gross could gain about €500 under a 10% rate or around €730 with full exemption.

- The measure remains under evaluation with scope, funding, and wording to be decided in the forthcoming budget law.