Overview

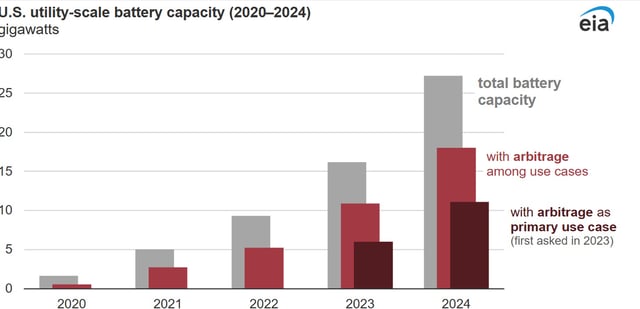

- Operators reported that 66% of utility-scale battery capacity had arbitrage among its uses and 41% was primarily used for arbitrage in 2024.

- Frequency regulation ranked second as the primary use at 24%, after previously being the most common application.

- The shift is captured by the EIA’s 2023 move to ask each operator for a single primary use, enabling clearer comparisons across the fleet.

- CAISO ended 2024 with 11.7 GW of battery capacity, 43% of which was primarily dedicated to arbitrage.

- ERCOT reported 8.1 GW of capacity with about half primarily used for arbitrage, underscoring where the trend is concentrated.