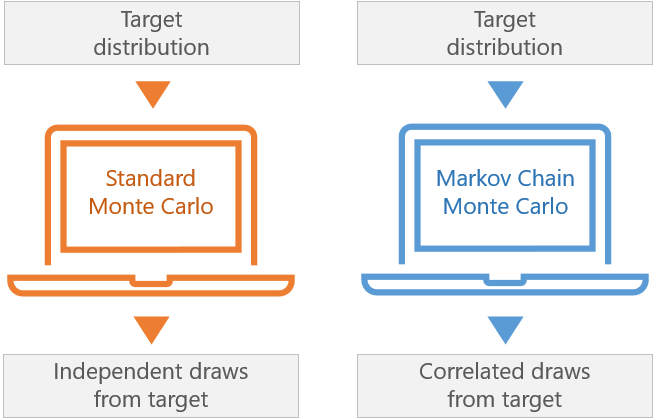

In statistics, Markov chain Monte Carlo is a class of algorithms used to draw samples from a probability distribution. Given a probability distribution, one can construct a Markov chain whose elements' distribution approximates it – that is, the Markov chain's equilibrium distribution matches the target distribution. From Wikipedia